Fiscal Imbalance in Canada Twenty Years after the Séguin Commission

Two decades ago, the Commission on Fiscal Imbalance, set up by the Quebec government, submitted its final report. The “Séguin Report” was an important milestone in the debate on fiscal imbalance that was raging in Canada at the time. A contemporary reading of the Commission’s writings reveals how many of its recommendations are still relevant today, and a divergence between the Commission’s recommendations and the evolution of fiscal arrangements since 2002. The current situation, as well as a number of blind spots in the Commission’s report, mean that a similar exercise looking at Canadian fiscal federalism in all its dimensions is needed today.

Two decades ago, the Commission on Fiscal Imbalance, set up by the Quebec government, submitted its final report, known as the Séguin Report.

A contemporary reading of the report reveals several points of convergence with the current fiscal situation. The report remains topical in part by identifying the institutional causes of fiscal imbalance, notably the exercise of the “federal spending power” whose legitimacy the Quebec government does not recognize. This new analysis also identifies discrepancies between the Commission’s recommendations and the evolution of financial arrangements since then, not least because certain current issues had not been anticipated in 2001-2002.

While an analysis of the report’s key recommendations shows that some have been adopted, such as technical modifications to the equalization formula, others such as the abolition of social transfers and the transfer of equivalent tax room, remain unimplemented.

New questions, an updated analysis

Despite the federal government’s current financial situation, which is different from that of the time, and the fact that fiscal federalism has evolved considerably since 2002, the Commission’s recommendations remain essentially relevant, but the analysis needs to be updated.

For instance, the current discourse of the provinces and territories generally focuses on an increase to social transfers; the consensus on this issue being easier to establish given the growth in healthcare spending. However, this new reading of the Séguin report shows that fiscal imbalance is a problem whose complexity cannot be summed up by the sheer scale of the chronic under-funding of social transfers.

If a similar consultation were to be held today, new questions would need to be answered. For example, should fiscal arrangements take into account the heterogeneity of spending needs between provinces, and thus move away from allocation on the basis of population alone? An update should also explore the possibility of revising the institutional framework to explicitly integrate the provinces into the decision-making process. Finally, this update should include a look at the role of Indigenous governments and the impact of natural resources on fiscal imbalance, two blind spots in the Séguin report.

Beyond these specific recommendations, the continuing relevance of the Séguin Report two decades later shows just how much the absence of a regular forum for reflection, discussion and analysis devoted to intergovernmental fiscal arrangements appears to be the primary flaw in Canada’s approach to fiscal federalism. Indeed, these issues tend to be discussed on an ad hoc and sporadic basis, with the occasional fever pitch in provincial capitals demanding more money from Ottawa.

In this sense, the Séguin Commission provides a powerful source of inspiration that undeniably deserves, two decades later, to be revisited and used as a starting point for a new exercise of its kind.

Introduction: 2002 and today — similarities and differences

A little more than 20 years ago, in March 2002, the Commission sur le déséquilibre fiscal (Commission on Fiscal Imbalance, CFI), created by the Quebec government under Premier Bernard Landry, produced its final report. The Séguin Report, named after commission president Yves Séguin, proved to be a major milestone in the debate over fiscal imbalance that was raging at the time, with the federal government running significant and growing budget surpluses (albeit after years of deficits) while the provinces continued for the most part to experience financial difficulties.

It would be easy to conclude that, with the return of deficits over the past few years, particularly at the federal level, the issue is settled and that there is no longer a fiscal imbalance. But it is at this juncture that the Séguin Report merits a contemporary rereading. Granted, the report is a product of its time, largely reflecting the era of budgetary surpluses under Jean Chrétien and Paul Martin. Yet it is certainly useful in highlighting the dynamics of public finances and the institutional causes of fiscal imbalance, notably the exercise of a “federal spending power” that the Quebec government does not recognize as legitimate. On these two points, the Séguin Report remains remarkably relevant.

Consider, for example, the COVID-19 pandemic. The health crisis, which in principle was within provincial jurisdiction, in fact saw the federal government deploy unprecedented financial resources in the health sector. In no time, Ottawa floated the imposition of federal conditions, notably in the sector of long-term care for seniors, a population that was hard hit at the start of the pandemic.

The recentralization of government action within federations is typical in periods of crisis. If the trendy concept of “polycrisis”[1] is an apt description of the new normal, then the federal government will not lack for opportunities to intervene in areas of provincial jurisdiction over the coming decades. This tendency was evident even before the pandemic (Graefe & Fiorillo, 2023), and was reinforced by the pact between the Liberals and the New Democrats (dental care, early childhood care, etc.). In line with the spirit of the Séguin Report, such an exercise of the “spending power” is a consequence of a fiscal imbalance.

We will therefore revisit the Séguin Report, two decades after its publication, with the main goal of examining its relevance today, as well as identifying some current issues that the commission’s work did not anticipate in 2001-2002. To achieve this goal, the text adopts a somewhat chronological, yet non-exhaustive approach in an attempt to answer the following questions:

- In what political and budgetary context was the commission created and its work carried out?

- What are the main elements of analysis, observations and recommendations contained in the Séguin Report?

- What do developments since the end of the CFI’s work tell us about its analysis, observations and recommendations?

- How can the Séguin Report’s blind spots serve as an analytical framework for the current situation?

The political and budgetary context

The debate over fiscal imbalance at the turn of the millennium originated, as seen from Quebec, in the intersection of two major trends marking the 1990s, one political — the national question — and the other budgetary — fiscal consolidation.

Politics

Politically speaking, it is difficult today to imagine how intense the period of constitutional debates was, culminating in the referendum on Quebec independence held October 30, 1995. Between deliberation over profound reform of the Canadian federation and plans for the establishment of an independent Quebec state, these were debates of a lofty nature, and current-affairs issues were magnified to historic proportions on a daily basis.

The referendum defeat of Jacques Parizeau’s Parti Québécois government marked, to a great extent, the apex of this period of impassioned debates on the future of the Canadian federation and abruptly closed the chapter that had (just as abruptly) begun with the failure of the Meech Lake Accord in June 1990.

In an acceleration of history such as we rarely experience, within just a few weeks at the end of 1995 the sovereigntist project met its Waterloo; Jacques Parizeau resigned as premier of Quebec; and Lucien Bouchard, former minister in Brian Mulroney’s cabinet, artisan of the Meech Lake Accord and founding leader of the Bloc Québécois since 1990, took control of the PQ and the Quebec government.

Public finances

Immediately upon taking office, Lucien Bouchard was confronted with Quebec’s significant budgetary challenges. Backed by its finance minister, Bernard Landry, the government’s focus shifted from a program aimed at achieving independence to one centred on achieving what was then called “zero deficit.”

The provinces were at the time suffering the fallout from federal transfer cuts, a situation dating back a few years to when the federal government, under pressure from international financial markets, embarked on its own rigorous fiscal consolidation to reduce the federal debt burden. The tough battle to achieve zero deficit, with cuts across all government functions, created public discontent and left a lasting mark on Lucien Bouchard’s two terms as premier.

Bernard Landry, who succeeded him on March 8, 2001, in a sense implemented a synthesis of the PQ’s political project, in which he had been a major player since the first government of René Lévesque in 1976, and contemporary finance issues, where he had been at the forefront since 1996 as finance minister. The establishment of the Commission on Fiscal Imbalance in 2001[2] perfectly embodied his desire to resume the great debates on Canadian federalism, placing the financial arrangements between the federal government and Quebec, and public finance issues more broadly, at the heart of the discussion.

The Commission on Fiscal Imbalance (2001-2002)

The commission was chaired by lawyer and tax expert Yves Séguin, a former minister (Revenue, Labour) in Robert Bourassa’s Liberal government from 1987 to 1990. After the commission, he was Minister of Finance in Jean Charest’s Liberal government from 2003 to 2005. The other members of the commission were lawyer Anne-Marie D’Amours, tax expert Renaud Lachance, lawyer Andrée Lajoie, economist Nicolas Marceau, political scientist Alain Noël, and lawyer Stéphane Saintonge. Its multidisciplinary composition (law, economics, political science, taxation) fit well with the broad definition of fiscal imbalance it was to embrace. The commission was supported in its work by a secretariat[3] based in Montreal, and the Ministère des Finances du Québec.

The commission submitted its final report on March 7, 2002, almost exactly one year after Bernard Landry became premier.[4]

Summary of the commission’s analysis[5]

The Séguin Report is structured in three parts:

- The nature of the problem;

- The causes of the fiscal imbalance;

- The consequences of the fiscal imbalance and the ways to respond.

This section deals with each of these elements in turn.

The nature of the problem

Fiscal imbalance is a complex problem. Before we can address what solutions are to be recommended for resolving it, it is important to define exactly what we mean by it. But first, we need to define an intermediate concept: the fiscal gap. Indeed, the fiscal imbalance, as addressed in the Séguin Report, refers to how this gap is filled by the financial arrangements between governments.

The fiscal gap

In all federations, there exists a fiscal gap, which is the difference between expenditures associated with the areas of responsibility of each level of government and their own sources of revenue. Depending on which countries or historical periods are being considered, this fiscal gap may favour the provinces or the federal government. In Canada, a fiscal gap favourable to the federal government emerged when the provinces “loaned” part of their fiscal space to Ottawa in 1942 to finance Canada’s participation in the Second World War (Commission on Fiscal Imbalance, 2002b).[6]

The fiscal gap is more difficult to estimate than it might appear at first. Indeed, the mere difference between budgetary expenditures and own-source revenues may underestimates the real fiscal gap. This is because a province’s current expenditures may underestimate the level of expenditures associated with its areas of jurisdiction.

On the one hand, a province may be unable to undertake certain expenditures that fall under its jurisdiction. These are “needs not covered” that do not appear in budgetary expenditures due to the government’s limited fiscal resources (A in table 1). As noted in the Séguin Report (Commission on Fiscal Imbalance, 2002a, p. 19), “the very existence of a fiscal imbalance can lead provinces to maintain a level of expenditures below their needs, given the insufficient financial resources at their disposal. Thus, there may be ‘needs not covered’ that must be taken into account in evaluating the fiscal imbalances, but which do not appear in the budget accounts.”

On the other hand, using the federal spending power, the federal government spends directly in the provinces’ areas of jurisdiction (B in table 1). Expenditures associated with needs not covered and with the spending power are therefore added to those associated with Quebec’s areas of jurisdiction in the calculation of the fiscal gap, which can be qualified as theoritical, in table 1.

How high are the amounts associated with needs not covered in Quebec’s areas of jurisdiction (A in table 1) and the federal government’s direct expenditures in Quebec’s areas of jurisdiction (B in table 1)?

By definition, needs not covered are very difficult to evaluate directly for a given year since they do not appear in the public accounts. However, they are indirectly revealed when pro forma projections of public finances are made. That’s what the Conference Board of Canada did for the CFI (Conference Board of Canada, 2002a). The Conference Board’s projections showed increasing deficits for the Quebec government over the next two decades, indicating a growing difficulty in covering the costs of public services observed at the time. Those rising deficits led the CFI to estimate “that Quebec should have annual additional financial resources of at least $2 billion in the short term and $3 billion in the medium term” (Commission on Fiscal Imbalance, 2002a, p. 133).

Implicitly, the CFI therefore estimated the variable A (in table 1), the non-covered needs, at between $2 billion and $3 billion per year, based on the Conference Board’s (2002a) projections for the fiscal years 2002-2003 to 2019-2020. This amount, increasing over the projection period, was projected to rise from 3.4 per cent of Quebec’s budget expenditures in 2002-2003 to 4.9 per cent in 2019-2020.

As for federal expenditures in Quebec’s areas of jurisdiction, the Secrétariat aux affaires intergouvernementales canadiennes estimated in 2002 that the new federal initiatives announced in the federal budgets from 1997 to 2000 alone amounted to more than $15 billion for all provinces (Commission on Fiscal Imbalance, 2002a, Figure 19, p. 112).

The vertical fiscal imbalance

There is a vertical fiscal imbalance when the fiscal gap is not adequately bridged. For it to be adequately bridged, the financial arrangements between provincial and federal governments must respect the principles of fiscal balance. The commission summarized these in three major principles (Commission on Fiscal Imbalance, 2002a, p. 14):[7]

- “First, sources of own-source revenue are allocated to each government, the resulting division of tax fields allowing each order of government sufficient financing to be accountable before its citizens for the decisions it has taken in its fields of jurisdiction.”

- “Second, total revenue, i.e. own-source revenue plus transfers, must enable each order of government to effectively cover the expenditures resulting from all the jurisdictions to be assumed.”

- “Thirdly, transfers from the federal government to the provinces must not limit the decision-making and budgetary autonomy of the provinces within their fields of jurisdiction, because of the conditions that accompany them or the way they are defined. This means that transfers should be unconditional unless the members of the federation have validly agreed to conditional transfers, for instance to promote the efficient operation of the federation.”

The CFI concluded that these three principles were not respected in the case of the Canadian federation, particularly in the financial relations between the governments of Quebec and Canada.

The horizontal fiscal imbalance

The phenomenon of fiscal imbalance also includes what is called horizontal fiscal imbalance. This refers to an inadequate correction for differences in fiscal capacity between provinces and territories. In Canada, the federal equalization program is responsible for balancing the fiscal capacities of the provinces (the territorial financing formula applies to the territories).

The causes of fiscal imbalance

After defining fiscal imbalance from a Quebec perspective, the Séguin Report turns to a three-chapter analysis of the causes of the phenomenon:

a) The imbalance between expenditures and access to sources of revenue;

b) Inadequate intergovernmental transfers; and

c) Federal spending power.

This section summarizes in turn the commission’s main findings on each of these “causes of fiscal imbalance.”

A growing fiscal gap that is inadequately addressed

For the commission, fiscal imbalance exists primarily because existing intergovernmental financial arrangements limit the provinces’ flexibility within their areas of jurisdiction. This results in non-covered needs, which become apparent when the current state of provincial public finances is projected into the future.

The commission’s analysis of the causes of fiscal imbalance had as a starting point the dynamics of expenditures in the respective areas of jurisdiction of the provinces and the federal government. In particular, the commission’s analysis highlighted the divergent dynamics between expenditures arising from the delivery of services (health, education, training, defence, etc.) and those arising from transfers (to individuals, businesses, or other levels of government). The analysis also underscored activity in fiscal jurisdictions tending to favour federal public finances over provincial ones. The commission concluded that responsibilities in terms of expenditures give rise to more significant long-term pressures on provincial public finances than on federal finances. If policies remained consistent, projections showed a progressive deterioration in provincial public finances and a progressive improvement at the federal level.

Inadequate federal transfers

The CFI contended that the fiscal imbalance of 2002 was also due to federal transfers being too often unpredictable, subject to federal government arbitrariness, and tied to federal conditions within the provinces’ areas of jurisdiction. The commission concluded that this state of affairs made provincial budget planning precarious and resulted in an accountability deficit.

Concerning horizontal fiscal imbalance in particular, the commission raised several issues that plagued the equalization program in 2002. The main issues were the use of the five-province standard,[8] the program’s unpredictability, and the arbitrariness that had crept in (particularly since the signing of special resource agreements between the federal government and Newfoundland and Labrador in 1985, and Nova Scotia in 1986[9]).

Exercise of federal spending power

Lastly, the commission viewed the exercise of a federal spending power as a manifestation of fiscal imbalance (Commission on Fiscal Imbalance, 2002a, 2002c). In other words, direct federal spending in areas of Quebec jurisdiction under federal spending power fails to respect the three principles of fiscal balance mentioned above: sufficient own-source revenues, total revenues covering spending-related expenditures, and federal transfers that do not constrain autonomy.

The solutions

According to the CFI, the three causes outlined in the preceding section are an integral part of the problem of fiscal imbalance and should all be dealt with within the framework of an eventual comprehensive solution. The commission’s report specifies that “fiscal imbalance is tied to the size of the fiscal gap between own-source revenue and spending, to the inadequacy of transfers to make up this difference, to the very characteristics of these transfers and to the ‛federal spending power,’ (Commission on Fiscal Imbalance, 2002a, p. 16).

The CFI’s main recommendations can be summarized into three elements:

- a) In order to correct the vertical fiscal imbalance, “social transfers” (known today as the Canada Health Transfer [CHT] and the Canada Social Transfer [CST]) must be abolished and replaced with a transfer of tax room;[10]

- b) To correct the horizontal fiscal imbalance, various changes to equalization payments are needed;

- c) Changes to the institutional context of intergovernmental financial arrangements are necessary to reduce federal arbitrariness in this sphere.

Abolishing “social transfers”

In line with the principles of fiscal balance, correcting the imbalance requires a reduction of the fiscal gap — which brings with it accountability issues — as well as implementing measures to significantly improve respect for the principles of autonomy and fiscal capacity in the way the federal government closes the remaining gap. In the spirit of the CFI’s analysis, resolving the fiscal imbalance involved replacing the CST and the CHT with a permanent transfer of federal government tax room to the Quebec government. As recommended by the commission, the transfer of tax room could occur both at the personal income tax level and at the level of the Goods and Services Tax.

Changes to equalization

Reform of equalization — which the commission viewed as complex, arbitrary in its calculation, and unpredictable — was also an integral part of the solution advocated by the commission. It proposed various changes to equalization, all essentially aimed at full compliance with the Representative Tax System (RTS), on which the program traditionally relies. Some of these recommendations are dealt with in the next section.[11]

Modifications to the institutional context of financial arrangements

Lastly, the CFI viewed certain institutional changes as indispensable for resolving the fiscal imbalance in a sustainable way. Putting an end to the arbitrariness of the federal government in this area requires that intergovernmental financial arrangements be jointly determined by the provinces and the federal government. In the current system, the federal government typically relies on consultations.

Correcting the fiscal imbalance also involves overseeing and limiting the federal government’s spending power in areas of provincial jurisdiction. Indeed, the commission saw a potential resolution of this imbalance as a way to limit such federal power by “reducing the financial leeway available for this purpose” (Commission on Fiscal Imbalance, 2002a, p. 153).

By including both vertical and horizontal fiscal imbalances as well as the institutions in charge of intergovernmental financial arrangements, the Séguin Report advocates for a comprehensive resolution of the fiscal imbalance, with the three solution axes mentioned above being essential and interrelated.

After the commission: the evolution of fiscal imbalance in Canada since 2002

After the tabling of the Séguin Report in 2002, the National Assembly unanimously endorsed its findings and recommendations. To what extent can subsequent developments be viewed as moving in their direction? We will now touch upon some of the major post-2002 changes to the financial arrangements through the lens of the commission’s recommendations.

Major developments since 2002

Fiscal federalism has evolved quite a bit since 2002. Firstly, the federal government has continued to unilaterally renew intergovernmental financial arrangements. These renewals, usually for five years, took place in 2002 (for the period 2004-2009), 2007 (for the period 2007-2014), 2013 (for the period 2014-2019), 2018 (for the period 2019-2024) and 2023 (for the period 2024-2029). The next one is therefore expected in 2029. Several other modifications took place between these renewals.[12]

The emergence of fixed-envelope equalization

The initial years following the commission’s work were marked by developments diametrically opposed to its recommendations. The federal government announced in 2004 that, for the 2004-2009 period, equalization would henceforth be funded through a fixed envelope (a cap), indexed annually at 3.5 per cent. It was in essence an abandonment of the traditional operation of the program (in place since 1982). In 2005, the Atlantic Accords were renewed.

The 2004-2009 renewal helped reignite the debate over fiscal imbalance. The Council of the Federation (2005) opposed the abandonment of the traditional operation of equalization, lamenting that it was now “based on a fixed envelope with a fixed escalator.”

The arrival of Stephen Harper at the helm of the federal government on February 6, 2006, marked a major turning point in the fiscal imbalance file. For the first time, a Canadian prime minister recognized that fiscal imbalance between the federal and provincial governments existed (Harper, 2006).

The “resolution of the fiscal imbalance” of 2007

A remodelling, announced in the federal budget of 2007 (Department of Finance Canada, 2007, p. 114 and following), took the form of a major reform of intergovernmental financial arrangements aimed at “restoring fiscal balance.” On equalization, the recommendations of the O’Brien Report (Expert Panel on Equalization and Territorial Formula Financing, 2006), implemented by the Harper government in 2007, included:

- Simplify the RTS: reduce the number of bases from 33 to 5, with only one for natural resources;

- Adopt the ten-province standard;

- Reduce the inclusion rate of natural resource revenues. The provinces now receive the higher amount resulting from a formula based on an inclusion rate of 50 per cent or 0 per cent;[13]

- End use of a fixed envelope;

- Introduce a smoothing mechanism for payments.

In addition to an equalization reform that adopted most of the O’Brien committee’s recommendations as well as a series of other measures, the March 19, 2007, budget announced two significant measures regarding social transfers: a 40 per cent increase in the CST envelope by 2008-2009 and the introduction of a per capita distribution for both the CST and CHT.

The result for Quebec was a total increase of $2 billion in 2007-2008 and $1.9 billion the following year, according to data from the May 2007 Quebec budget. Soon after his re-election that same year, Jean Charest’s government used the additional financial leeway resulting from the resolution of the fiscal imbalance to reduce personal income tax, announced in the May 2007 budget. Almost all the provinces implemented tax cuts around the same time (Ministère des Finances du Québec, 2007).

The GDP ceiling

In November 2008, Ottawa announced the return to a fixed indexed envelope based on a three-year moving average of nominal Canadian GDP growth (the “GDP ceiling”). Transition protection payments ensured that the transfers received by a province did not decrease from one year to the next.

The financial arrangements established in 2007 and amended in 2008 essentially remain in effect today. They were renewed in 2013 and 2018. During that time, there was a noticeable calming of the debate over fiscal imbalance (Joanis, 2023) before it started up again, driven initially by Alberta and Saskatchewan.

Recent developments

In recent years, particularly in the context of the COVID-19 pandemic, issues related to fiscal imbalance have returned to the forefront. Among recent federal announcements, we note the reform of the fiscal stabilization program announced in the fall of 2020; a one-time increase in health transfers announced in March 2021; and the finalization of “an unconditional Asymmetrical Childcare Agreement of $6.0 billion over five years, from 2021-2022 to 2025-2026,” according to the terms of the 2022-2023 Quebec budget (Ministère des Finances du Québec, 2022).

Assessment of the commission’s main recommendations

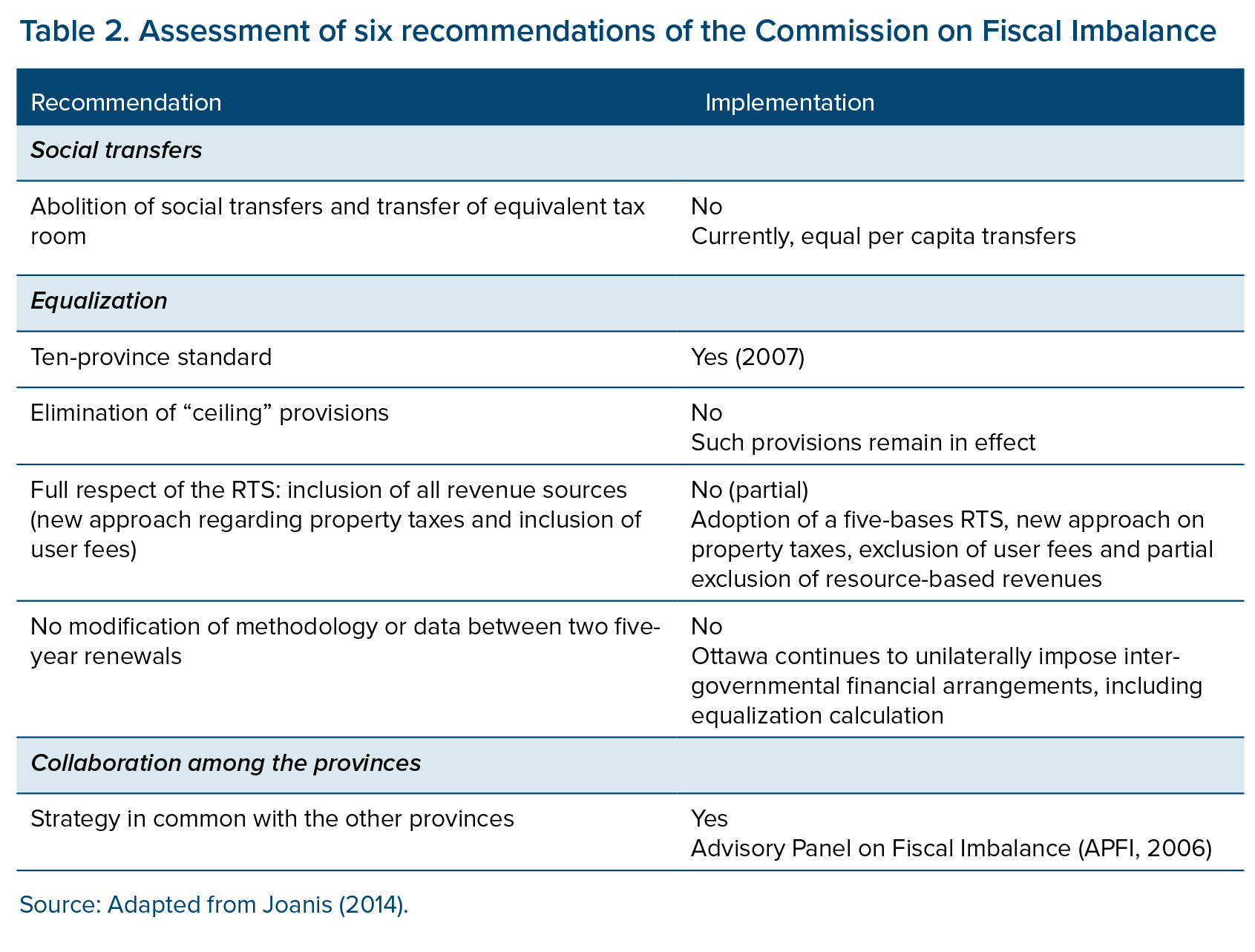

We will briefly focus here on three groupings of the commission’s recommendations: the evolution of social transfers, changes to equalization, and provincial co-operation on issues related to financial arrangements between the federal and provincial governments. Table 2 presents a list of six of the commission’s recommendations.

Social transfers

The CFI adopted the provincial premiers’ “traditional position” on fiscal imbalance, namely that the value of the federal government’s social transfers (today the CHT and CST) was insufficient for the provinces to adequately fulfil their constitutional responsibilities in these areas. To correct this situation, the provinces had indeed long been asking that the federal government’s share of financing of provincial spending in health, post-secondary education and income security be restored to the level it was at before the federal cutbacks in the middle of the 1990s.

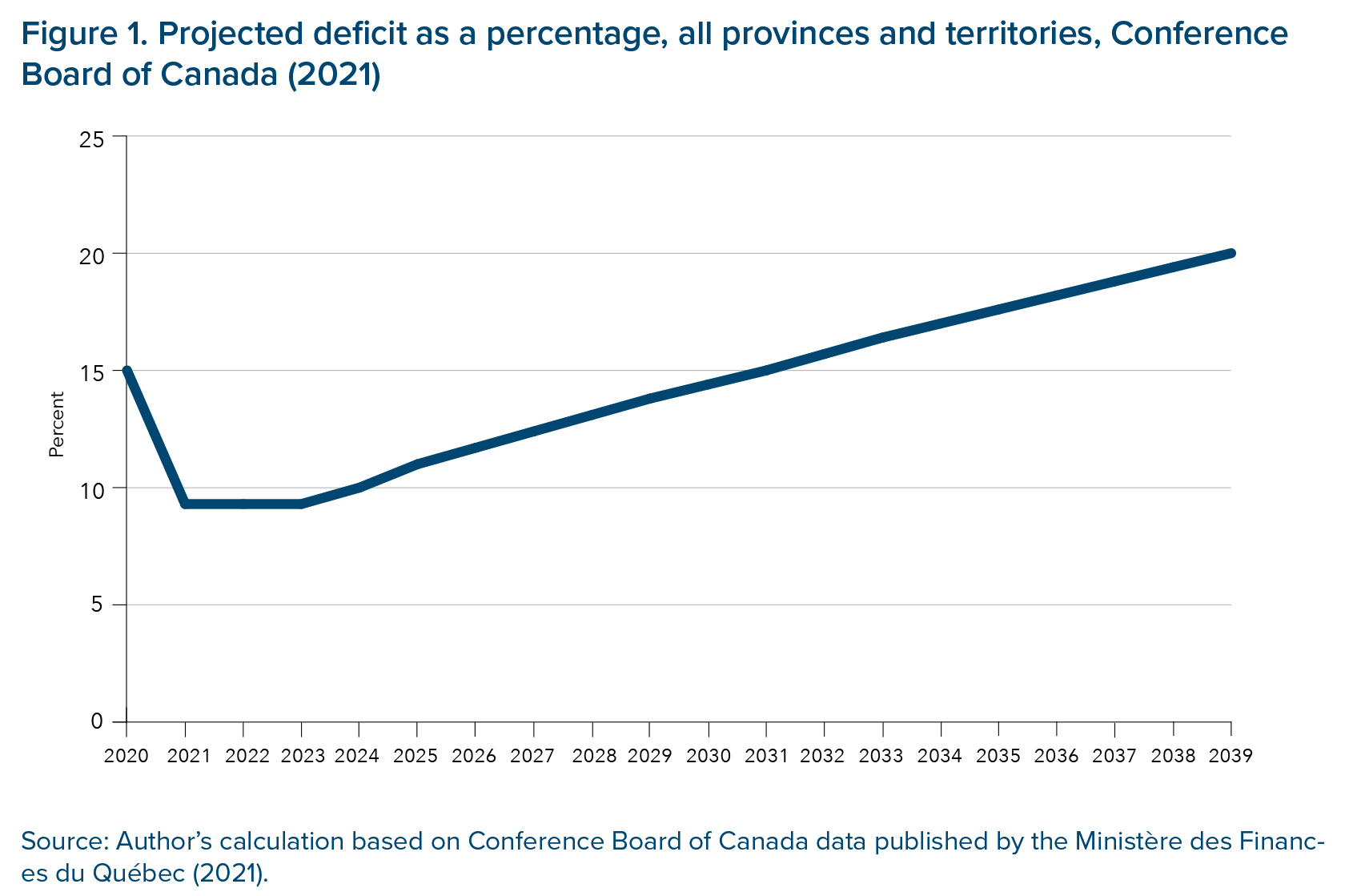

With respect to the level of social transfers, it is more than clear that, as the saying goes, the more things change, the more they remain the same. The Council of the Federation continues to demand an increase in health transfers so that they represent 35 per cent of the health expenditures covered by the CHT. Results from a Conference Board of Canada forecasting exercise included in Quebec’s 2021-2022 budget (Ministère des Finances du Québec, 2021) indicate a significant increase in the projected budget deficits for all provinces and territories; the deficits are projected to rise from 15 per cent of budget expenditures in 2019-2020 to 20 per cent in 2039-2040 (figure 1).[14]

However, for the CFI, correcting the fiscal imbalance undoubtedly involved the resumption of social transfers to re-establish the share of federal funding to levels prior to the cutbacks of the 1990s. But — more importantly — it called for the eventual replacement of the transfers by a permanent transfer of tax room. The CST and CHT are of course still in place today, although they were revised in 2007 and in subsequent years so as to be allocated on an equal per capita basis, a feature that still corresponds to the current situation.

Equalization

Despite the many changes implemented in 2007 following the O’Brien Report, adoption of the principle of a fixed equalization envelope (GDP ceiling) — first adopted in 2004, suspended in 2007 and then reintroduced in 2008 — represents a departure from the traditional functioning of equalization that goes against the commission’s recommendations Overall, the existing equalization program has moved away from full compliance with the RTS — notably by reducing the number of bases and the partial exclusion of natural resources — and currently looks more like a political compromise. Moreover, Ottawa continues to unilaterally impose intergovernmental financial arrangements, including the entire equalization calculation methodology.

It is, however, important to note that some technical improvements to the program introduced in 2007 directly address concerns raised in the Séguin Report:

- A more predictable functioning of short-term equalization (smoothing mechanism);

- A new approach on property taxes; and

- The ten-province standard.

Collaboration among the provinces

Following the commission’s emphasis on a shared strategy with the other provinces, the Quebec government exercised a strong leadership in establishing the Council of the Federation in 2003 and in its repeated advocacy in subsequent years for a resolution of the fiscal imbalance. An interprovincial consensus on the fiscal imbalance issue was quickly hammered out, formalized by the creation of the Advisory Panel on Fiscal Imbalance (APFI 2006). The Council of the Federation’s work (APFI, 2006)[15] helped make fiscal imbalance a central issue of the 2006 federal election campaign.

The provinces and territories generally focus their demands on a significant increase in social transfers. That’s where a consensus is easiest to establish, even more so today with rising health care expenditures. However, a rereading of the Séguin Report indicates that fiscal imbalance is a problem whose great complexity cannot be summarized by the notion of chronic underfunding of social transfers. Thus, as with many other similar issues in the past, the fiscal imbalance as defined in the Séguin Report poses a significant challenge for a “united front” of the provinces.

Indeed, the solutions chosen to address the fiscal imbalance depend on the perspective one adopts, particularly regarding the division of powers between different levels of government.[16] Quebec’s definition of fiscal imbalance — contained in the Séguin Report, as described above — does not always correspond with that of officials in other provinces. The positions set out over the years by the Ontario government (Courchene, 2005) nicely illustrate the diverse perspectives that can emerge from different provinces. While the commission adopted a “provincial perspective” on the fiscal gap, the Ontario government has tended to adopt a “federal perspective.” Thus, Ontario places significant importance on the gap between federal revenues and expenditures within a single province (including federal transfers).[17] Such an approach does not directly address the issue of respecting the provinces’ constitutional powers, which is central to Quebec’s approach.[18]

Partly owing to the differing definitions of fiscal imbalance that may circulate in provincial capitals, the solutions naturally preferred by each province are disparate. The less affluent provinces, with the exception of Quebec, are generally reluctant to support the transfer of tax room, as a “tax point” is worth less in a “have-not” province than in a “have” one. In Quebec, successive governments have generally decided, as the CFI did, that the financial disadvantage in certain cases of the transfer of tax room (as opposed to a cash transfer) is more than offset by gains in fiscal autonomy and funding predictability. Furthermore, Quebec and the “rich provinces” — which receive no equalization payments — generally place more importance on vertical fiscal imbalance than on horizontal fiscal imbalance, whereas the opposite is true in the other provinces.

In short, the joint strategy with the other provinces regarding the fiscal imbalance, as recommended by the CFI, was indeed implemented starting in 2002. However, in order to continue, the strategy was gradually narrowed down to simply demanding an increase in social transfers. Most of the commission’s recommendations were not adopted, either by provincial consensus or by the federal government. Still, some recommendations of a technical nature, specifically those related to equalization, have been implemented since 2002: the ten-province standard, the smoothing mechanism, property taxes, etc.

Blind spots in the Séguin Report

The two previous sections highlighted areas of convergence between the current situation and the findings of the Séguin Report, as well as a lack of alignment between the commission’s recommendations and the evolution of financial arrangements since 2002. This suggests that, for the most part, the analysis of the Séguin Report remains valid today. However, a contemporary rereading also reveals, in retrospect, a number of blind spots.

Natural resources

Perhaps the most surprising blind spot of the Séguin Report is the limited attention given to natural resources and their impact on the evolution of the horizontal fiscal imbalance. The analysis of the natural resource issues is primarily limited to the offshore resource agreements benefiting Newfoundland and Labrador and Nova Scotia. The commission held “that such ad hoc solutions raise problems of equity among the recipient provinces and run counter to the very spirit of the program that offsets relative disparities among the provinces” (Commission on Fiscal Imbalance, 2002a, p. 101).

Over the last two decades, the fiscal and political dynamics of the federation have evolved significantly in tandem with oil and gas prices. Ever since 2002, Newfoundland and Labrador has convincingly demonstrated that it is possible to transition from a “have-not” province to a “have” province. Despite this, not only have the offshore agreements been renewed and maintained for an extended period, but the treatment of natural resources in equalization has been completely revised, including the introduction of 50 per cent inclusion rate in the calculation. More generally, equalization has evolved since 2002 in a way that reduces its responsiveness to the evolution of the horizontal fiscal imbalance resulting from changes in the natural resources sector.

According to the CFI, equalization should continue to be based as much as possible on a comprehensive RTS, including as many of the revenue sources used by the provinces as possible. At the time of the commission’s analysis, 33 tax bases were modelled and considered in the equalization calculation. Following the recommendations of the O’Brien committee, the federal government opted in 2007 to simplify the RTS, reducing it from 33 to 5 tax bases. Four of these — personal income tax, corporate income tax, consumption taxes and property taxes — have continued to be treated according to the traditional operation of the program, but the fifth — natural resources — underwent a complete change in approach.

Revenues derived from resources present measurement challenges not to be trivialized. In the spirit of the Séguin Report, approaches targeting a single issue (offshore resources, electricity rates, etc.) should be avoided in favour of comprehensive solutions based on the principles of fiscal balance.

Resource revenues tend to increase the horizontal fiscal imbalance and create upward pressures on the cost of the equalization program for the federal government, which seeks to shield itself from these pressures as much as possible. This problem is becoming increasingly pronounced in Canada with the booming fiscal capacity of provinces producing oil and natural gas.[19]

Crises and recentralization

Many observers seem to think that the world we live in is increasingly characterized by a succession of crises. Yet, both experience and the literature on the subject identify crises (wars, economic depressions, etc.) as vehicles of (re-)centralization (Canavire Bacarreza et al., 2021).

The recent COVID-19 pandemic was no exception. In the short term, it increased vertical fiscal imbalance by intensifying existing pressures on health-care spending, especially in the provinces. In response to the crisis, the federal government resorted to one-time increases in the CHT. However, the current federal government also seems to de facto consider health as a shared jurisdiction, openly contemplating direct interventions in the field like national standards for long-term care in addition to transfers. The supply and confidence agreement between the New Democratic Party and the Liberals on March 22, 2022, contained several points in this regard, including some programs announced since then, such as the new dental care program.

Others

The Séguin Report also showed other blind spots, such as local and Indigenous governments, the role of the territories in fiscal arrangements (not addressed by the CFI), and climate change. There is therefore a need to update the analysis from both a Quebec and a pan-Canadian perspective.

Conclusion: AN EXERCISE TO BE UPDATED

The most recent pro forma projections of federal and provincial public finances reveal that the dynamics between the two levels of government are similar to those prevailing in the early 2000s (favouring the federal government in the long term). Since the provinces are responsible for the strategic sectors of health and education, their expenditures will increase more rapidly than their revenues in the coming years. The opposite is true for the federal government: its expenditures tend to grow more slowly than its own-source revenues over a long period. The current distribution of revenue sources between the federal government and the provinces will therefore result in a growing fiscal gap in the coming decades, a pointed illustration of fiscal imbalance.

Yet the starting point is much different from what it was in 2002, mainly due to the recent COVID-19 crisis, which led to a major deterioration in federal finances in the short and medium term. More broadly, it is worth noting that the exercise of public finance projections over the long term has become considerably more uncertain (at least in the short term).

More fundamentally, the federal government has the initiative in determining intergovernmental financial arrangements. This allows it to largely insulate itself from pressures on federal transfers. On the equalization front, the federal government can insulate itself from an increase in the horizontal fiscal imbalance by imposing “ceiling” provisions. With regard to health and social program transfers, it is insulated from an increase in vertical fiscal imbalance by a now complete abandonment of a cost-sharing mindset. The provinces, though, face uncertainty regarding the future evolution of transfers, stemming both from the unilateral nature of federal decisions concerning fiscal arrangements and from the very nature of how the programs operate (complex system of calculation, etc.).

Despite the current federal government’s financial situation, the CFI’s recommendations are still relevant today, but the analysis needs updating. An update should include addressing the blind spots listed in the previous section. It should also answer new questions, including the following, which merit in-depth analysis:

- Should federal public finances be insulated from financial pressures related to the volatility of provincial fiscal capacities? In other words, isn’t it normal for equalization to become more expensive when the horizontal fiscal imbalance increases?

- Should fiscal arrangements take into account the differences in spending needs between the provinces, thus shifting away from a distribution among provinces based solely on population?

- Would a simplified equalization (“macro approach” rather than RTS) better withstand political pressures?

- How can the institutional framework be revised so that the provinces can be expressly incorporated into the decision-making process? Is an enhanced role for the Council of the Federation possible? Could we draw inspiration from what is done elsewhere?

In previous publications (Joanis, 2014, 2018), I recommended three potential mechanisms that I continue to find relevant today:

- An independent body for managing fiscal arrangements — The federal government is under constant political pressure, both from voters and from the provinces, leading to periodic ad hoc changes to fiscal arrangements. Everyone would no doubt benefit from a less political and more rational approach to fiscal arrangements. The Australian model, with its Commonwealth Grants Commission, is often mentioned as an interesting example (Commission on Fiscal Imbalance, 2001).

- Pre-financing the equalization program — The existing institutions governing fiscal arrangements have not been able to protect the provinces from unilateral decisions by the federal government. In addition to entrusting transfer programs to an independent body, another option might be considered: partially pre-financing the equalization program. An equalization fund with predetermined, anticipated federal contributions, separate from the federal budget, would help insulate the program from the federal government’s cyclical cost-cutting decisions while making the program’s financing more predictable for Ottawa. Such a solution would be difficult to implement without an independent body.

- A macro approach to equalization — Though the RTS approach is in principle desirable, the experience in recent decades has shown how politically challenging it is to apply it in full (revenues from natural resources, etc.). The constant technical debates over the handling of various specific cases (hydroelectric revenues, property taxes, etc.) generate opportunities for parallel agreements motivated by political considerations and unequal treatment between provinces. This adds to the well-known disadvantage of the RTS approach: its lack of transparency makes it nearly impossible for anyone outside a small circle of insiders to understand exactly where the annual changes come from. A simpler and less controversial approach should perhaps be considered: a macroeconomic approach to estimate fiscal capacities based on a small number of indicators.

Apart from these specific recommendations, it is perhaps the absence of a regular forum for reflection, discussion and analysis dedicated to intergovernmental fiscal arrangements that stands out as the primary shortcoming of the Canadian approach to fiscal federalism. These issues tend to be discussed on an ad hoc and sporadic basis, with occasional flare-ups in provincial capitals involving demands for more money from Ottawa. The latest five-year renewals of fiscal arrangements by the federal government were practically done behind closed doors.

While continuity in this area can be appreciated in some respects, many substantive issues would benefit from being discussed publicly in a structured, rigorous and recurring framework, leading — where necessary — to the reforms that are required after analysis. This is why the Séguin Commission is a strong source of inspiration that undeniably deserves attention two decades on. A contemporary reading of the commission’s work reveals several parallels with the current situation but also, inevitably, a number of blind spots inspiring us to undertake today, in similar spirit, a renewed reflection on Canadian fiscal federalism in all its aspects.

[1] On this topic, see for example Whiting and Park (2023).

[2] The announcement was made by Premier Bernard Landry in the National Assembly on March 22 and the order in council adopted on May 9.

[3] It should be noted that I was part of the secretariat, a freshly arrived economist from the Department of Finance Canada. The secretariat also relied on the services of full-time economic and tax analystes, including Suzie St-Cerny, Luc Godbout, David Boisclair, David Bard and myself. It is worth noting that several subsequent collaborations grew out of our intense interactions in the Montreal secretariat (it was a pleasure to have been a co-author at different times with Suzie, Luc and David Boisclair in the years following the commission’s work). Among the commissioners, it is worth mentioning that two of them went on to serve as Quebec’s finance minister (Yves Séguin, from 2003 to 2005, and Nicolas Marceau, from 2012 to 2014). Renaud Lachance became Quebec’s auditor general and later a commissioner on the Commission of Inquiry into the Tendering and Management of Public Contracts in the Construction Industry (the “Charbonneau Commission”). Among secretariat members, Luc Godbout would for his part be called on to chair the Taxation Review Committee (his “Godbout Report” was published in 2015).

[4] His mandate as premier ended on April 29, 2003, after the defeat of the Parti Québécois at the hands of Jean Charest’s Liberals.

[5] This section is in part an update of previous texts: Joanis (2006a, 2006b, 2011).

[6] According to Linteau et al. (1989, p. 164), under this agreement, from 1941 to 1947 the federal government collected $2.26 billion in Quebec and returned only $103 million.

[7] The CFI did not name these principles, although its report contains a discussion of them (Commission on Fiscal Imbalance, 2002a, p. 14). As stipulated by the commission, these “principles” all stem from the application of the “federal principle” (p. 13). Godbout and Dumont (2005) add the principles of “predictability” and “interdependence and cooperation” to the list.

[8] Quebec, Ontario, Manitoba, Saskatchewan and British Columbia.

[9] The Atlantic Accords on offshore oil and gas were intended to protect the offshore oil and gas revenues until those provinces had notably improved their economic situation. The accords allowed Newfoundland and Labrador and Nova Scotia to keep 100 per cent of the revenues from offshore resources so long as they received equalization payments.

[10] A transfer of tax room occurs when, in a co-ordinated and explicit fashion, one level of government reduces its taxation level on one tax base and another government level increases it proportionally.

[11] For a more in-depth discussion of equalization issues between 2002 and 2014, see Joanis (2014).

[12] For a list of the major changes to equalization and social transfers in each year, see the online appendix in Joanis (2018).

[13] The addition of a 0 per cent option to the 50 per cent compromise of the O’Brien Report was inspired by the Conservative Party’s electoral promise to completely exclude revenues from non-renewable natural resources from the equalization calculations.

[14] For comparison’s sake, the Conference Board (2002b) conducted a similar exercise in July 2002 for all provinces and territories. The results for all provinces and territories allowed for the following calculation: that the ratio of a projected fiscal balance to expenditures would rise over the projected period, similar to Quebec (above), rising from 0.3 per cent in 2002-2003 to 3.2 per cent in 2019-2020. Besides the Conference Board, many organizations and researchers regularly conduct this type of fiscal sustainability analysis. For a recent discussion in the Quebec context, see Jacques et al. (2023).

[15] The Advisory Panel on Fiscal Imbalance, co-chaired by Robert Gagné and Janice Gross Stein, published its report on March 31, 2006. Also on the panel were Peter Meekison, Lowell Murray and John Todd.

[16] Boadway (2004) also shares this viewpoint.

[17] It is important to note that while this gap is generally positive for the most affluent provinces, it is generally negative in the case of the othe Equalization-receiving provinces. Indeed, the federal government normally spends more in Quebec than it collects in revenues. Federal spending in Quebec of course includes federal spending in Quebec areas of jurisdiction, which makes this calculation a matter of political sensitivity in the province. Also notable is the fact that this calculation is typically based on provincial economic accounts, published by Statistics Canada, rather than data from public accounts (used by the CFI and in this Insight). The accounting standards used by Statistics Canada can also result in divergent interpretations of these results.

[18] Regarding this issue, see the commission’s argument (Commission on Fiscal Imbalance, 2002a, p. 17), which insists on “what constitutes one of the true sources of the problem, namely the distribution of powers and of the spheres of taxation.”

[19] For a more in-depth discussion of current federal fiscal issues related to natural resources, see Joanis and Vaillancourt (2020).

References

Advisory Panel on Fiscal Imbalance (APFI). (2006). Reconciling the irreconcilable: Addressing Canada’s imbalance. Council of the Federation.

Boadway, R. (2004). Should the Canadian federation be rebalanced? Working Paper 2004-1. University of Western Ontario, Economic Policy Research Institute.

Canavire-Bacarreza, G., Evia Salas, P., & Martinez-Vazquez, J. (2021). The effect of crises on fiscal and political recentralization: Large-panel evidence. Working Paper 21-11. International Center for Public Policy, Andrew Young School of Policy Studies, Georgia State University.

Commission on Fiscal Imbalance. (2001). Intergovernmental fiscal arrangements: Germany, Australia, Belgium, Spain, United States, Switzerland. Background paper. Gouvernement du Québec.

Commission on Fiscal Imbalance. (2002a). A new division of Canada’s financial resources. Commission report. Gouvernement du Québec.

Commission on Fiscal Imbalance. (2002b). Fiscal imbalance in Canada — Historical background. Supporting document 1. Gouvernement du Québec.

Commission on Fiscal Imbalance. (2002c). The “Federal Spending Power.” Supporting document 2. Gouvernement du Québec.

Commission on Fiscal Imbalance. (2002d). Texts submitted for the International Symposium on Fiscal Imbalance. Supporting document 3. Gouvernement du Québec.

Conference Board of Canada. (2002a). Projection of financial balances of the governments of Canada and Quebec. Document prepared for the Commission on Fiscal Imbalance.

Conference Board of Canada. (2002b). Projection of financial balances of the governments of Canada and of the provinces and territories. Conference Board of Canada.

Council of the Federation. (2005, August 12). Communiqué [Press release].

https://www.canadaspremiers.ca/wp-content/uploads/2017/09/communique_aug12.pdf

Courchene, T. J. (2005). Vertical and horizontal fiscal imbalances: An Ontario perspective. Presentation to the Standing Committee on Finance of the House of Commons, Institute for Research on Public Policy.

Department of Finance Canada. (2007). The 2007 budget plan. Government of Canada.

Expert Panel on Equalization and Territorial Formula Financing. (2006). Achieving a national purpose: Putting equalization back on track. Government of Canada.

Godbout, L., & Dumont, K. (2005). Mettre cartes sur table pour résoudre le déséquilibre fiscal. Série Scientifique du CIRANO 2005s-28. Chaire de recherche en fiscalité et en finances publiques de l’Université de Sherbrooke.

Graefe, P., & Fiorillo, N. (2023). The federal spending power in the Trudeau era: Back to the future? IRPP Study 91. Institute for Research on Public Policy.

Harper, S. (2006, April 20). Prime Minister Harper outlines his government’s priorities and open federalism approach [Speech]. https://www.canada.ca/en/news/archive/2006/04/prime-minister-harper-outlines-his-government-priorities-open-federalism-approach-207899.html

Jacques, O., Joanis, M., & Turcotte, J. (2023). Soutenabilité budgétaire du Québec et vieillissement de la population: implications pour la révision de la Loi sur la réduction de la dette. 2023PR-01. CIRANO.

Joanis, M. (2006a). Un test crucial pour les institutions du fédéralisme canadien. In L. Godbout (Ed.), Agir maintenant pour le Québec de demain (pp. 187-198). Presses de l’Université Laval.

Joanis, M. (2006b). Tirer profit de la nouvelle donne fédérale-provinciale: Vers un règlement du déséquilibre fiscal. Memo prepared for the Secrétariat aux affaires intergouvernementales canadiennes du Québec.

Joanis, M. (2011). Les politiques publiques à l’ère du “fédéralisme flexible.” In S. Paquin, L. Bernier, & G. Lachapelle (Eds.), L’analyse des politiques publiques (pp. 337-354). Presses de l’Université de Montréal.

Joanis, M. (2014). The politics of chequebook federalism: Can electoral considerations affect federal-provincial transfers? SPP Research Papers. The School of Public Policy, University of Calgary.

Joanis, M. (2018). The politics of chequebook federalism: Can electoral considerations affect federal-provincial transfers? Public Finance Review, 46(4), 665-691.

Joanis, M. (2023). Living on equalization payments: How hard is it for receiving provinces to anticipate future equalization revenues? In A. Lecours, D. Béland, T. Tombe, & E. Champagne (Eds.), Fiscal federalism in Canada: Analysis, evaluation, prescription (pp. 132-154). University of Toronto Press.

Joanis, M., & Vaillancourt, F. (2020). Federal finance arrangements in Canada: The challenges of fiscal imbalance and natural resource rents. In S. Yilmaz & F. Zahir (Eds.), Intergovernmental transfers in federations (pp. 109-133). Edward Elgar Publishing.

Linteau, P.-A., Durocher, R., Robert, J.-C., & Ricard, F. (1989). La mutation du fédéralisme. In P. Linteau, R. Durocher, J.-C. Robert, & F. Ricard (Eds.), Histoire du Québec contemporain, Tome II: Le Québec depuis 1930 (pp. 157-166). Éditions du Boréal Express.

Ministère des Finances du Québec. (2007). Budget 2007-2008: Plan budgétaire. Gouvernement du Québec.

Ministère des Finances du Québec. (2021). Budget 2021-2022: Pour un financement fédéral accru en santé. Gouvernement du Québec.

Ministère des Finances du Québec. (2022). Budget 2022-2023: Plan budgétaire. Gouvernement du Québec.

Ministère des Finances du Québec. (2023). Budget 2023-2024: Plan budgétaire. Gouvernement du Québec.

Whiting, K., & Park, H. (2023, March 7). Health and healthcare systems: This is why ‘polycrisis’ is a useful way of looking at the world right now. World Economic Forum.

https://www.weforum.org/agenda/2023/03/polycrisis-adam-tooze-historian-explains/

This study was published as part of the research of the Centre of Excellence on the Canadian Federation, under the direction of Charles Breton and assisted by Ji Yoon Han. The manuscript was proofread by Zofia Laubitz, editorial co-ordination was by Étienne Tremblay, production was by Chantal Létourneau and art direction was by Anne Tremblay.

This text was translated from French by Bertrand Marotte. The original French version of this text is available under the title Le déséquilibre fiscal au Canada vingt ans après la Commission Séguin.

Marcelin Joanis is a full professor at Polytechnique Montréal, where he is a member of the Groupe de recherche en Gestion et mondialisation de la technologie (GMT) and Deputy Director of the Michael D. Penner Institute on Environmental, Social and Governance Issues (ESG) on the Université de Montréal campus. He is CIRANO Researcher and Fellow and was a member of the Secretariat of Commission on Fiscal Imbalance.

This study is part of the Centre of Excellence on the Canadian Federation’s “L’idée fédérale” series, which aims to better understand and analyse Canadian federalism from a Quebec perspective.

To cite this document:

Marcellin, J. (2024). Fiscal Imbalance in Canada Twenty Years after the Séguin Commission. IRPP Insight No. 60. Institute for Research on Public Policy.

The opinions expressed in this paper are those of the author and do not necessarily reflect the views of the IRPP, its Board of Directors or sponsors. Research independence is one of the IRPP’s core values, and the IRPP maintains editorial control over all publications.

IRPP Insight is a refereed series that is published irregularly throughout the year. It provides commentary on timely topics in public policy by experts in the field. Each publication is subject to rigorous internal and external peer review for academic soundness and policy relevance.

If you have questions about our publications, please contact irpp@irpp.org. If you would like to subscribe to our newsletter, IRPP News, please go to our website, at irpp.org.

Illustration: Istock

ISSN 2291-7748 (Online)